The biggest trending topics in Nigeria since the new year began has been focused on the subject of tax.

People are suddenly careful with bank transfer narrations. There's new advice everywhere you turn about what you shouldn't write as your narration. Screenshots, Broadcast messages are being shared on different groups and social media, and there’s a sort of panic about how the new Nigerian tax law works.

Questions are being asked in hushed tones:

“Will transfers from my bank account be taxed?”

“Should I add a narration so the government doesn’t think it’s income?”

“If I flip my crypto to Naira on FlipEx, will tax be deducted?”

“Please add ‘gift’ as the narration before you send the money for my gift card trade to my account!”

Behind all this anxiety is one thing: Nigeria’s new tax act 2025 or Nigeria’s new tax law.

There seems to be a lot of misinformation flying about concerning Nigeria’s New Tax Act and how it will be administered. Most of the fear surrounding the new tax law is not coming from the law itself; It’s coming from misunderstanding.

So, this article intends to help you slow things down, clear the noise, and explain clearly what Nigeria’s new tax law actually says, what it does not say, and why panic is the wrong response to the new tax act. Where necessary, we will quote the law itself and link to the official source so you can see for yourself.

What is Nigeria’s New Tax Law? And Who Does It Affect?

In June 2025, President Tinubu signed four tax reform bills into law. One of the tax reform bills signed is the Nigeria Tax Act (NTA), 2025 which takes effect from January, 2026. The Tax Act was formulated by a Presidential Fiscal Policy and Tax Reforms Committee led by Mr. Taiwo Oyedele as part of a broader tax reform effort aimed at simplifying how taxes work, closing loopholes, and bringing clarity to modern income systems, particularly digital income in Nigeria.

The reform harmonises:

- Personal income tax rules

- Business and enterprise taxes

- Digital and online income recognition

At its core, the question new Nigerian Tax Law is asking is:

Who is earning taxable income in today’s Nigeria, and how can the system be fairer and clearer?

Will Bank Transfers Be Taxable Under Nigeria’s New Tax Law?

No. Your bank transfers will not be taxed. Under Nigeria’s New Tax Law, tax deductions will only be from money that represents income, profit, or gains.

According to Section 3 of the Nigeria Tax Act, 2025:

“Income tax shall be determined in accordance with the provisions of this Act, and imposed on the—

(a) profits or gains of any company or enterprise;

(b) income of any individual or family;

(c) income arising, accruing or due to a trustee, or an estate.”

Section 4 further defines taxable income:

“Income, profits or gains… includes —

(a) profits or gains from any trade, business, profession or vocation,

(b) salaries, wages, fees, allowances, compensations, bonuses, benefits,

(c) dividends, rents, interest, royalties, etc.,

(d) profits or gains from disposal of property,

(e) profits or gains from transactions in digital or virtual assets,

(f) prizes, winnings, honoraria, awards.”

No part of the New Tax Act says the urgent 2k you transfer between your friends or family, or any other deposits into your account will be taxed. Only the income you make will be taxed.

How to Calculate Income Tax with Nigeria’s New Tax Law in 2026?

Again, tax will only apply to your income and not the total amount that moves through your bank account. The process is as follows:

- Identify income - Whether it is from your salary, business profit, professional fees, or even your winnings from games, etc.

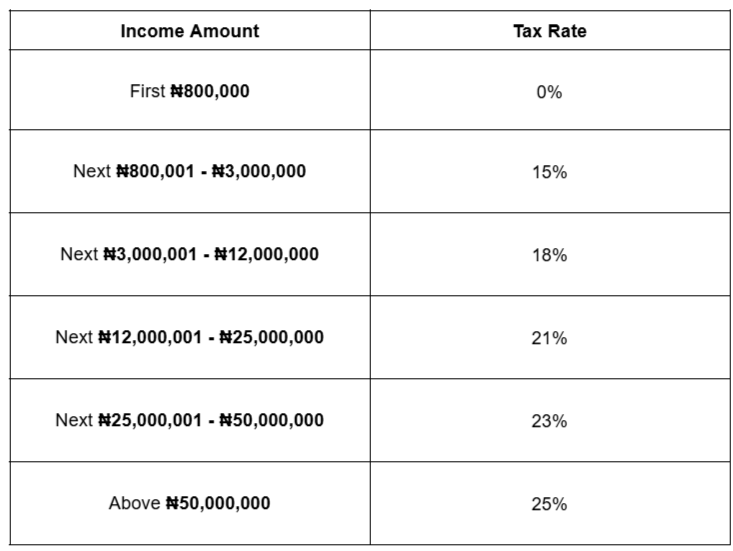

- Apply exemptions - Section 58 of the Tax Act sets a tax-free threshold of ₦800,000 per year for individuals so the first ₦800,000 will attract zero tax.

- Subtract allowable deductions - The New Tax Act also accommodates specific deductions such as pension contributions, National Health and Housing Insurance, Rent relief, and other approved reliefs. So, all of these will be deducted from the total income too.

- Apply progressive tax rates - The remainder of the total income after the zero tax ₦800,000 and the deductibles will then be taxed according to the rates in the tax bands.

The rates are as follows:

All these four steps are necessary and must be completed to determine the final amount to be paid as tax.

Sample Tax Calculation for a Middle-Income Nigerian

Suppose Mr or Mrs Bello earns ₦250,000 monthly, their annual earning will be ₦3,000,000 (₦250,000 * 12)

Let us calculate their payable tax together:

- The first ₦800,000 will attract 0% tax → not taxed. Taxable Income Balance will be ₦3,000,000 - ₦800,000 = ₦2,200,000.

- For the remaining Taxable ₦2,200,000 → we will apply deductions such as rent relief up to 20% of annual rent or ₦500,000 maximum. So, if Mr or Mrs Bello’s annual rent is ₦1,000,000, they will be entitled to getting rent relief of ₦200,000 which will be deducted from the Taxable Income Balance. The new Taxable income balance will now remain ₦2,200,000 - ₦200,000 = ₦2,000,000.

- If their Pension, Health Insurance equals another ₦500,000, then the new Taxable income balance will be ₦2,000,000 - ₦500,000 = ₦1,500,000.

- The remaining Taxable income balance of ₦1,500,000 will now be taxed by applying the progressive tax rates. Since ₦1,500,000 falls within the range of ₦800,001 - ₦3,000,000, a 15% tax will be the final amount payable as tax by Mr or Mrs Bello.

15% of ₦1,500,000 = ₦225,000

Mr or Mrs Bello will pay ₦225,000 as their annual income tax. This will amount to ₦18,750 monthly.

No part of the tax calculation makes reference to Mr or Mrs. Bello’s bank transfers and their narrations. The question to ask then is - what role do bank transaction narrations then play?

How does Bank Transfer Narrations Affect Tax?

Bank transfer narrations play an important role in helping you to keep track of monies as they move in and out of your bank account. The narration on any bank transaction will neither exempt nor subject such transaction to tax.

To calculate your tax, The Nigerian Revenue Service (NRS) formerly Federal Inland Revenue Service (FIRS) will calculate your tax from the income that you declare. They will then compare your declared income with the economic reality and your bank records. So, in reality your bank records will simply play an assessment role with the tax authorities. The tax authorities in carrying out their assessment can check your declared income and run comparisons between your declared income and your income sources.

If the tax authorities believe that there’s a disparity in your declared income and your actual income, the tax law provides laid down penalties and fines for tax related offences. So, adding narrations to your bank transactions is a good practice that will help you know how your money is being spent, but they will not be applied to calculating your tax. Using narrations can help improve the transparency of your bank transactions but it would not prevent taxation. Clear bank records will only help to verify your declared income.

Who Needs to Know About Nigeria’s New Tax Law 2026?

Every Nigerian should be abreast of the changes and introductions to the tax law. Nigerians earning income, especially digital income should understand how the new tax law provisions apply to them.

This new tax law is particularly relevant for:

- Salary earners

- Freelancers and consultants

- Side hustlers

- Digital income earners

- People trading gift cards, crypto and other digital assets on online platforms like FlipEx

The applicable provisions under the new tax law takes care of both high and low income earners and provides a fair tax rate based on each income category.

FAQs on Nigeria’s New Tax Law 2026

Will I be taxed on every transfer I send or receive under the new tax law?

No. Only your income, gains, or profits will be taxed, not the amount that you send or receive.

Will my bank account be blocked if I don’t get a Tax Identification Number (TIN)?

No. Your BVN and NIN can be used in place of a TIN. Provided you have a BVN and NIN, you can continue to operate your bank account.

Does a transaction narration exempt me from paying tax?

No. Tax authorities will not consider transaction narrations when assessing your tax obligations. They will check your declared income and your income sources.

Will I pay tax on loans?

No. You will not pay tax on any loan. The bank or financial institution that issues the loan will pay tax on the income generated via the loan.

How are deductions and exemptions applied in Nigeria’s new tax law 2026?

There are allowable deductions such as pensions, insurance, and rent reliefs provided under the new tax law. The approved reliefs must be claimed and documented before they can be applied to tax deductions and calculations.

How much will I earn to pay 0% tax?

The tax-free threshold is ₦800,000 per year.

Are crypto earnings taxable under Nigeria’s new tax law?

Yes. The new tax laws recognize digital assets so, the income, profit, or gains that are made from trading your crypto, gift cards and other digital assets are subject to tax under the new tax act.

Read more about our in-depth explanation of crypto tax in Nigeria.

If my family abroad sends me money, will the government deduct tax?

No. Money sent to support friends and family will not be taxed as those monies will not be regarded as income. Family and friends working abroad will pay taxes in the countries where they live and work already. But if you earn money abroad, maybe as a freelancer or staff of an international company while you are in Nigeria, that qualifies as income and will be taxed.

Why Understanding Nigeria’s New Tax Law Matters

Nigeria’s new tax law is a step toward transparency and fairness. By understanding the law, reading the cited sections, and interpreting them correctly, you can manage your tax responsibilities calmly and confidently.

Drowning in all the fear and misinformation will create more panic rather than clarity. It is imperative to understand what the New tax law says, understand its structure, system, rules, and punishments.

If you have any questions concerning the new tax law, you can reach out to our support desk, and we will provide all the help you need to fully understand the new tax laws and how it applies to you.

You can also read more blogs from FlipEx to understand what this new tax law means for digital finance users — including those trading gift cards and crypto.